Summary

Client: MiBolsillo App

Sector: Fintech

Challenge: Develop an in-app credit score builder (B2B/B2C)

My Role: User Experience Researcher and Interface Designer

Background Research

Before starting with the design journey, I scrapped data from World Bank’s Global Findex and Cepal to better understand how to develop a product, including every country's regulations (score), that can be useful to people and profitable to our company.

Also, I obtained data from the percentage of the population that’s banked but has not access to credit.

Competitor Analysis

Various financial institutions, lenders, and fintech companies in Latin America offer credit builder tools.

These tools help individuals establish a credit history or improve their credit profiles.

While specific providers may vary across countries, here are some standard credit builder tools available in Latin America.

-

Many financial institutions offer secured credit cards where individuals provide a deposit as collateral to secure a credit limit. Individuals can build credit by using these cards responsibly and making timely payments.

-

Description text goes here

-

Financial institutions and microfinance organizations provide credit-builder loans that are specifically designed to help individuals establish credit. These loans often have lower loan amounts and affordable repayment terms.

-

Fintech companies in Latin America have emerged with innovative credit builder tools. They often leverage technology and alternative data sources to assess creditworthiness and offer loans or credit-building services to individuals with limited credit history.

-

Retailers in Latin America may offer their own credit cards, making it easier for individuals to access credit. By using these cards responsibly, individuals can establish a credit history.

-

Some organizations provide credit education programs and resources to help individuals understand credit management, improve financial literacy, and develop good credit habits.

It's important to note that the availability and specific providers of credit builder tools can vary by country within Latin America.

The Design Process

After my market research and considering the time frame and resources, I decided to organise the steps towards the solution under the first four phases of the Design Thinking methodology umbrella.

I selected this in favour of the other, faster methods because I seek to understand the users, challenge any assumptions, fine-tune the problem and create an innovative solution.

Design Thinking revolves around a deep interest in understanding the people for whom we’re designing the products or services - it helps us observe and develop empathy with the target user.

The goals I will pursue through the 4 phases of Design Thinking are as follows:

ⓐ Empathise - conducting user interviews.

ⓑ Define – extracting the users’ insights. Building data-based personas.

ⓒ Ideate – creating a user flow that can be feasible and usable.

ⓓ Prototype – from wireframes to high fidelity mockups

Empathise: Interviews

I have selected people from our user database from countries included in the rollout of the new feature.

The interviewees came from different economic backgrounds. I wanted to get insights from users regarding their banking and borrowing money experiences.

I invited the users via e-mail and push notifications. I have listed some of the key insights from the interviewees below ↓

User interviews key insights

-

Users highlighted their desire to improve their credit scores despite being rejected in the past. They were looking for qualifying for better loan terms, working capital, or applying for a mortgage. They expressed the importance of having a tool that not only tracks their progress but also provides actionable steps to enhance their creditworthiness.

-

Several participants expressed the desire for seamless integration with their bank and credit card accounts. They saw value in having all financial data in one place, enabling a comprehensive view of their financial health and facilitating the identification of areas for improvement.

-

Users expressed the need for educational content within the app, including articles, videos, and tutorials that provide guidance on credit management, budgeting, and debt reduction strategies. They appreciated resources that empower them to make informed financial decisions.

-

Many users expressed a lack of knowledge about credit scores and how they are calculated. They emphasised the need for clear explanations and educational resources within the app to help them understand the factors that impact their credit scores.

-

Users highlighted the importance of a user-friendly interface that simplifies complex credit-related information. They appreciated intuitive navigation, visual representations of credit progress, and easy-to-understand explanations of credit-related terms.

Based on the results of the interviews phase. I modelled the following personas ↓

Define: Personas

Alice Goldsmith

-

Age: 45

Education: Undergraduate

Hometown: Montevideo, Uruguay

Family: Married with children

Occupation: Small business owner

Mobile Platform: Android

-

She’s a passionate and determined woman who ran a delightful food stall in the bustling heart of a vibrant market in Montevideo. She welcomed customers from all walks of life with a warm smile and a hearty greeting. Alice's stall was a treasure trove of flavours, offering various homemade dishes and mouthwatering delicacies.

-

Driven by her ambition, Alice is embarking on a mission to secure a loan to provide her with the necessary capital to grow and transform her food stall into a restaurant.

-

Alice tried to apply for a loan, but there were so many requirements that she did not meet.

The banks always seem overwhelming, and she instead gets the money from a small financial institution.

Rachel Clapich

-

Age: 31

Education: Massage therapist

Hometown: Rosario, Argentina

Family: Single with a cat

Occupation: Works in a mall massage service.

Mobile Platform: Android

-

Rachel is a skilled and compassionate massage therapist who dreams of opening her own small practice. Rachel had spent years perfecting her craft, honing her skills, and building a loyal clientele. Now, she was ready to take the next step in her career and create a space to provide healing and relaxation to even more clients.

-

Driven by her passion for helping others and her entrepreneurial spirit, Rachel set out to secure a loan to turn her dream into a reality.

She understood that opening a practice would require significant upfront costs, including renting a suitable location, purchasing equipment and supplies, and marketing her services.

-

Financial institutions have many rules for providing loans to small businesses, particularly service-based ones like Rachel's massage practice. They expressed concerns about the unpredictable nature of the industry, the lack of collateral, and the perceived high-risk associated with startups.

Despite facing rejection and disappointment, Rachel refused to give up on her dreams. She understood that the traditional banking system might not be the only avenue to explore.

Ideate: User Flow

I mapped out the primary path of the user flow. I involved multiple teams in the mapping. It guided stakeholders about how this tool should work and ensure our users achieve their goals efficiently. You can see the complete picture here or by clicking on the image.

Prototype: Wireframes

These wireframes outline the design's essential features, such as navigation, content layout, and functionality. These wireframes served as a guide for the team and help ensure that everyone was on the same page regarding the design.

-

![]()

Splash Screen 1

-

![]()

Splash Screen 2

-

![]()

Amount Input Screen

-

![]()

Address Screen

-

![]()

Income Screen

-

![]()

Residential Status

-

![]()

Dependents Screen

-

![]()

Review Screen

Prototype: High Fidelity

After the research process and analysis of existing products, I gained a deep understanding of the target audience's needs and preferences.

I kept the user's goals and needs in mind as I designed each screen, ensuring the flow was logical and easy to navigate. I also incorporated design elements to make the tool engaging and visually appealing.

-

![]()

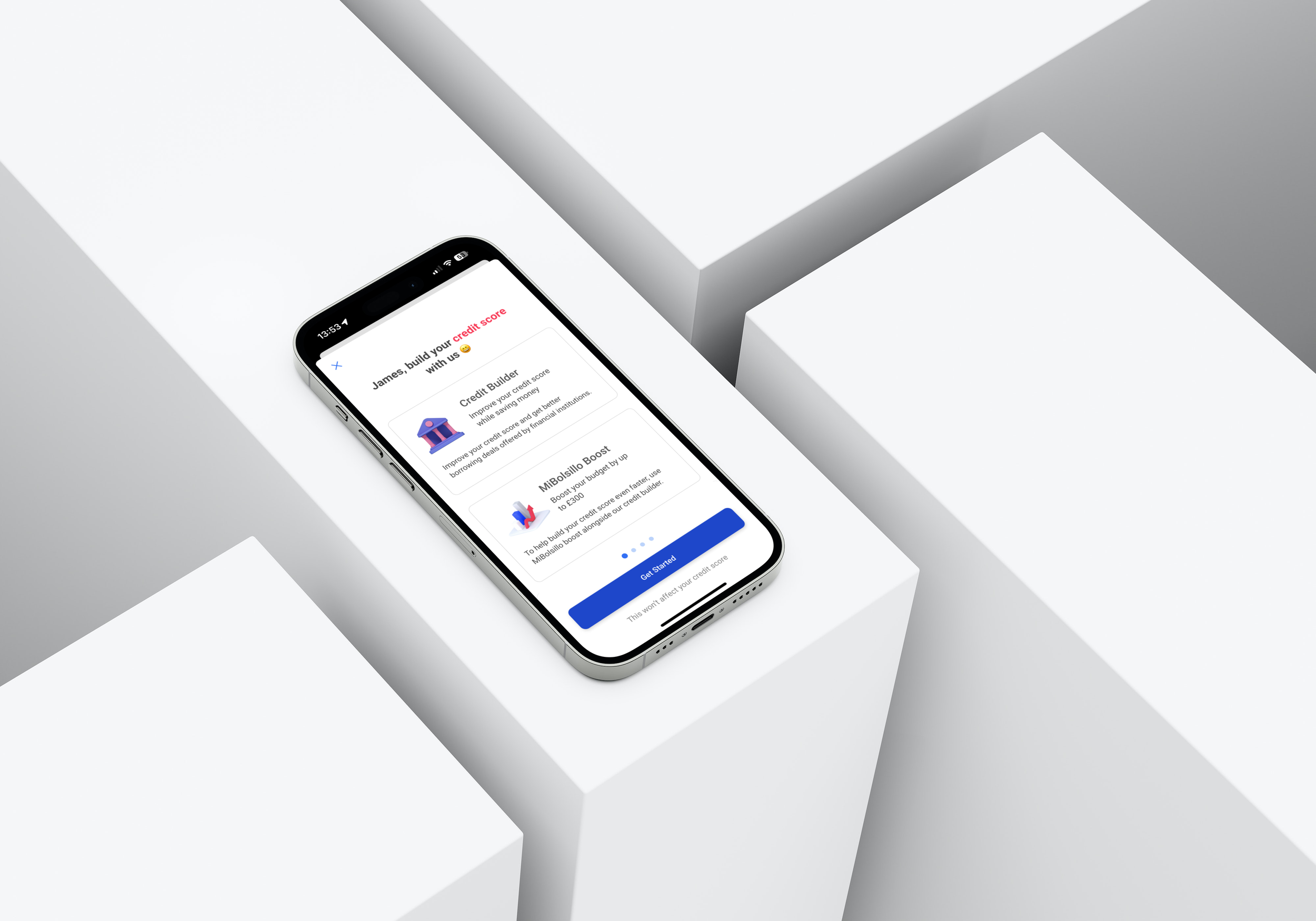

Welcome Screen

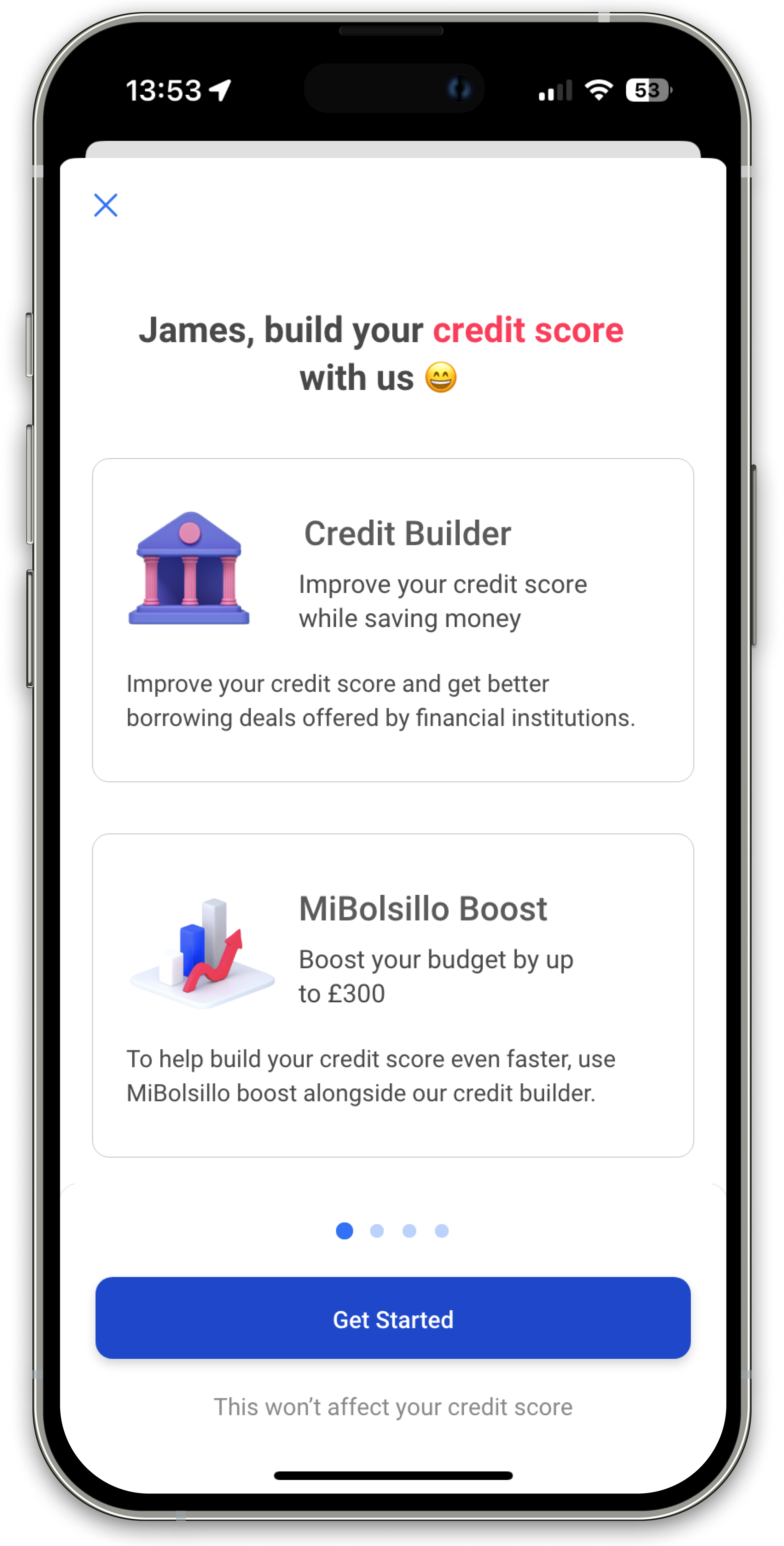

This screen provides the option to go directly to the credit builder or use the budget wizard.

-

![]()

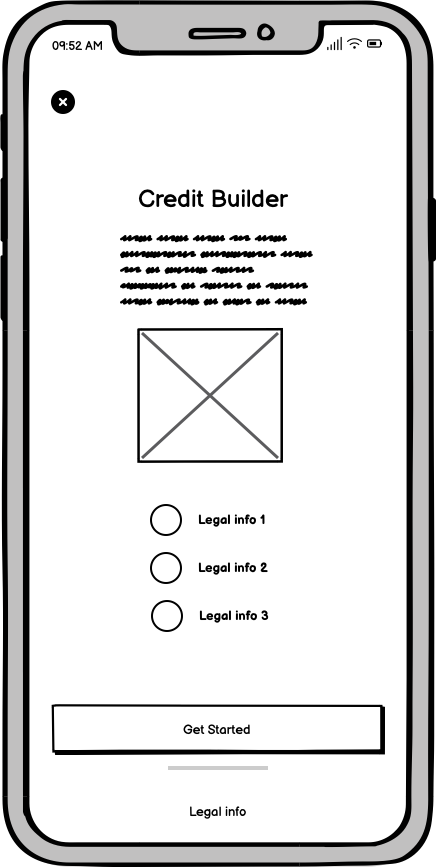

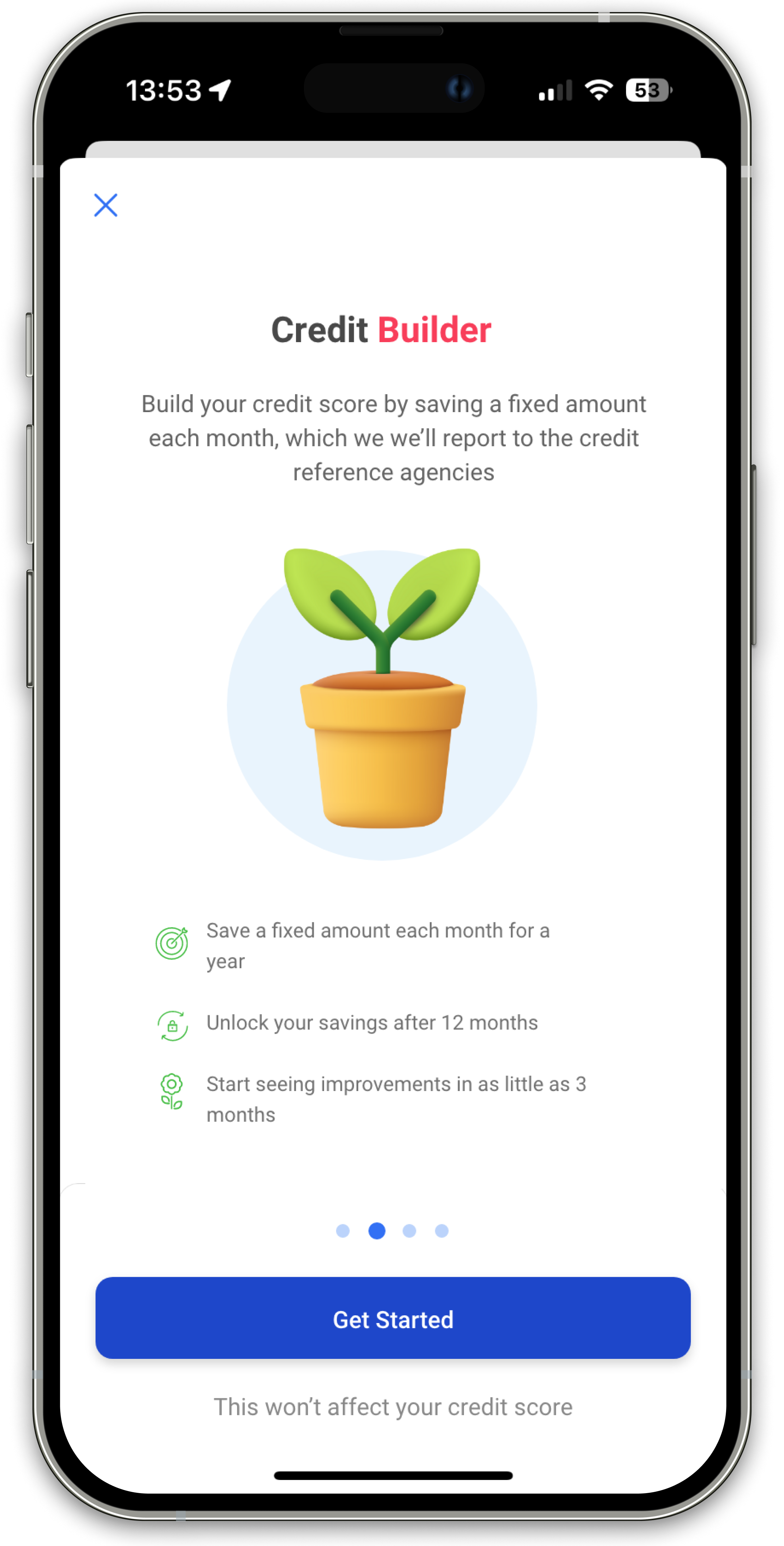

Splash Screen

This screen provides all the info the user needs to know prior to start the process.

-

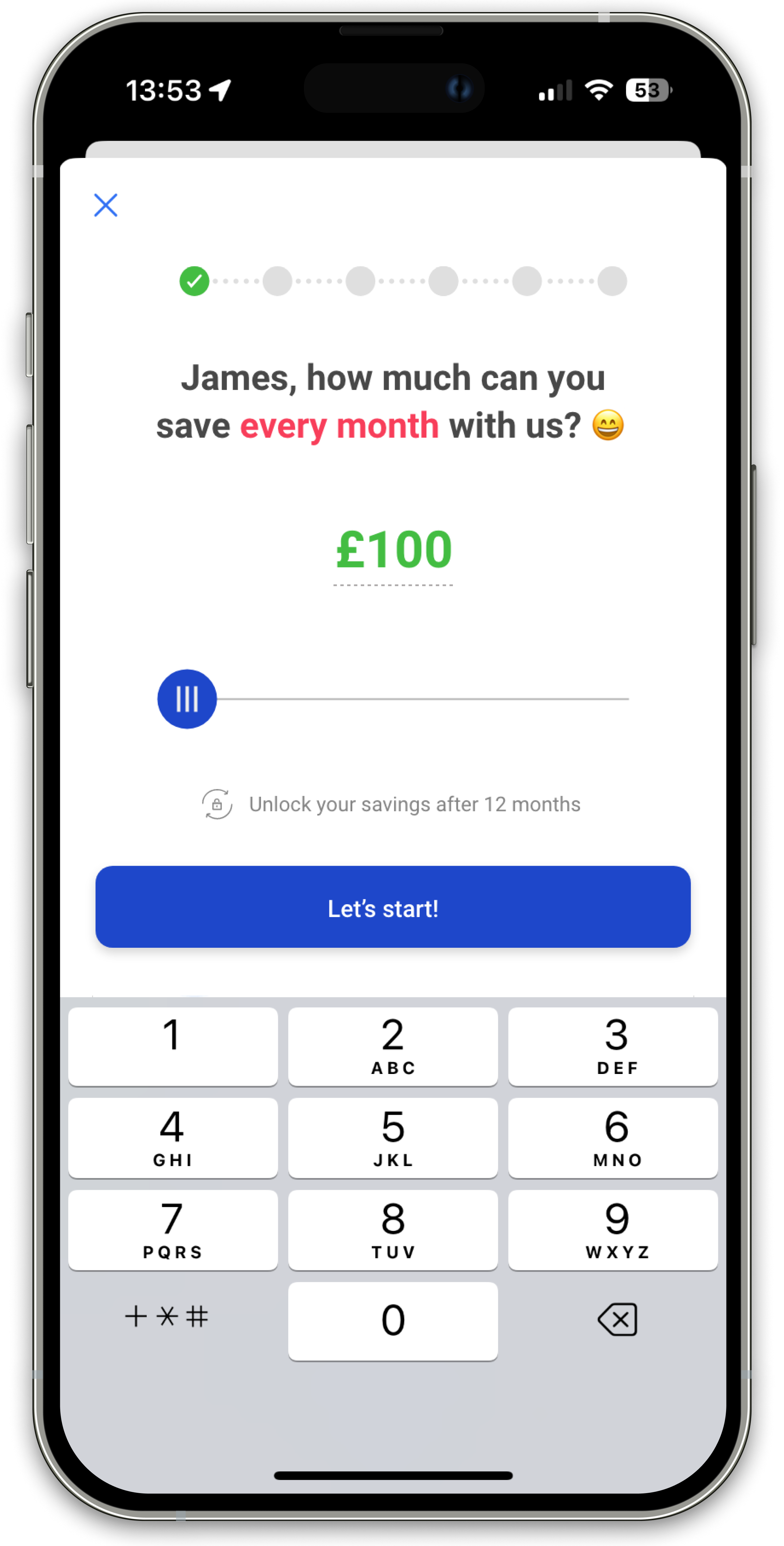

![]()

Amount Screen

I used an anchor to hint user what is the minimum they need to save per month.

-

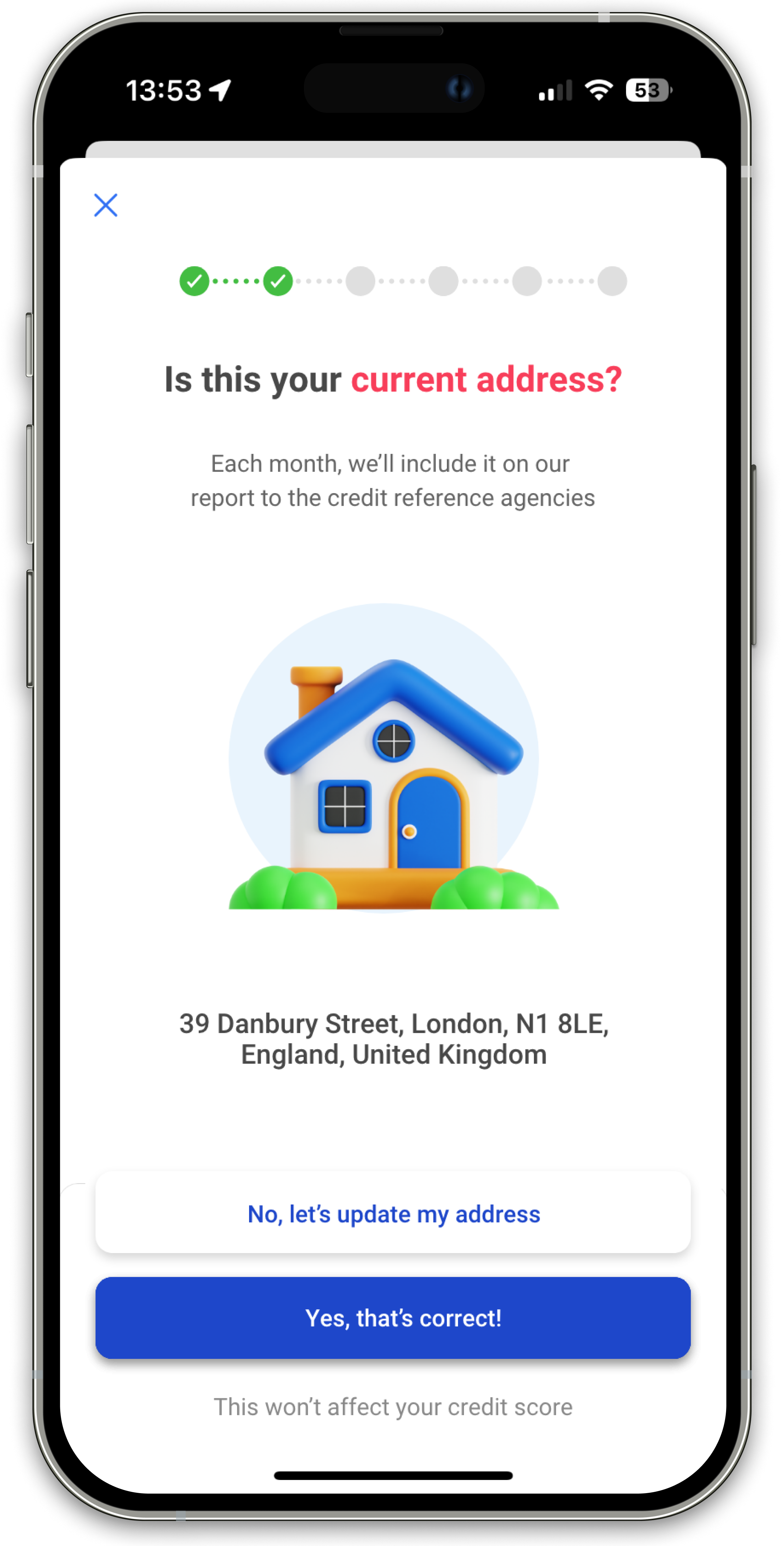

![]()

Address Screen

I explain why the user need to provide this info. I pulled the data previously added by the user to make it even faster.

-

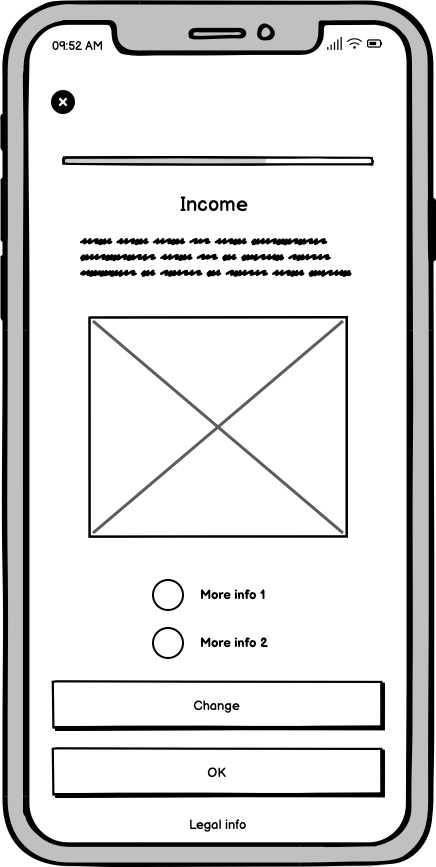

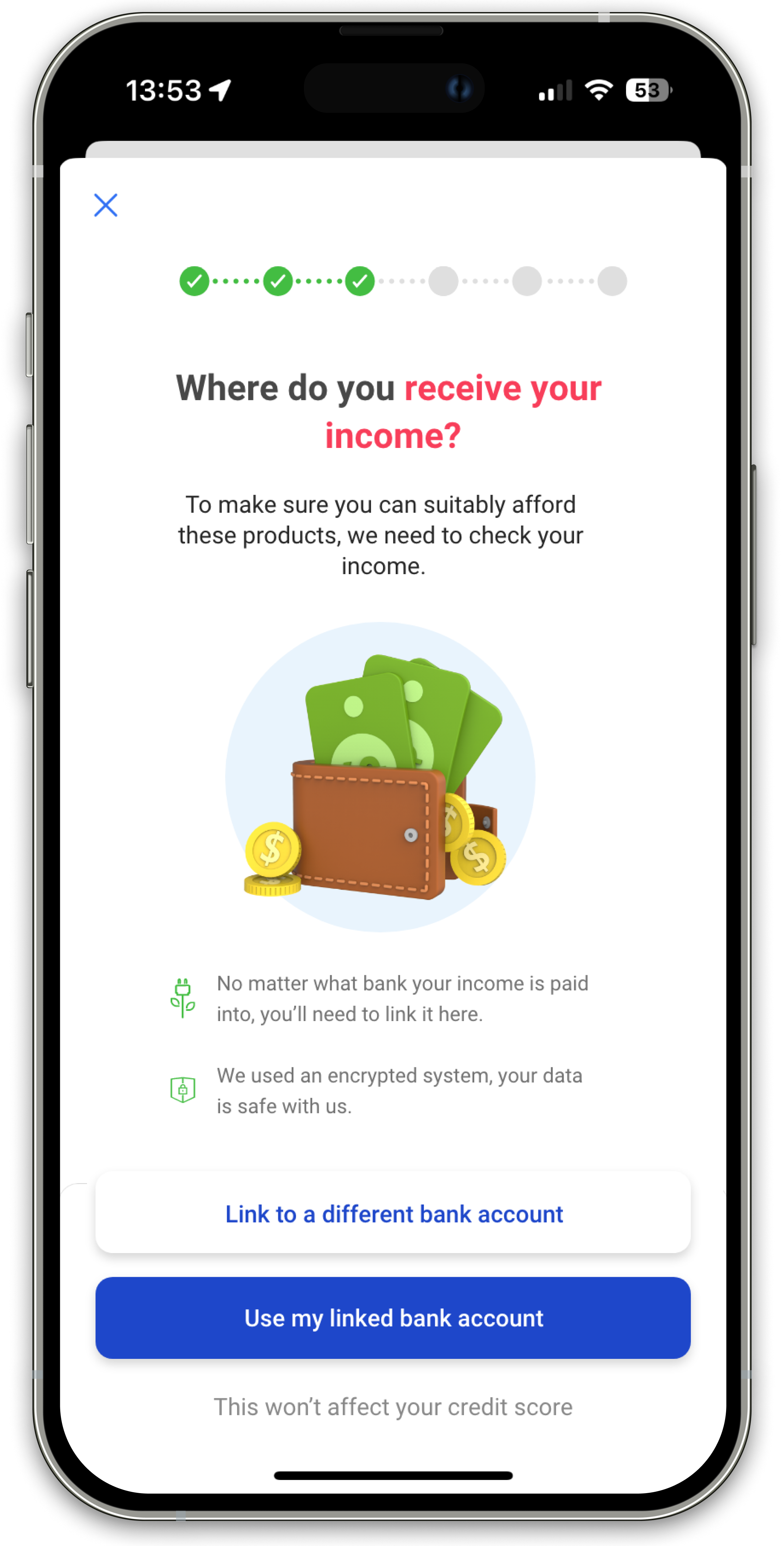

![Income Screen]()

Income Screen

-

![]()

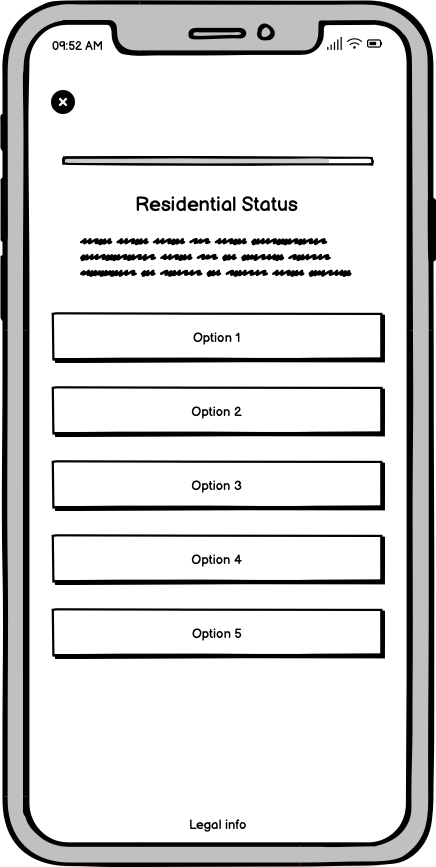

Home Ownership

According to regulations, the user needs to confirm their resident status.

-

![]()

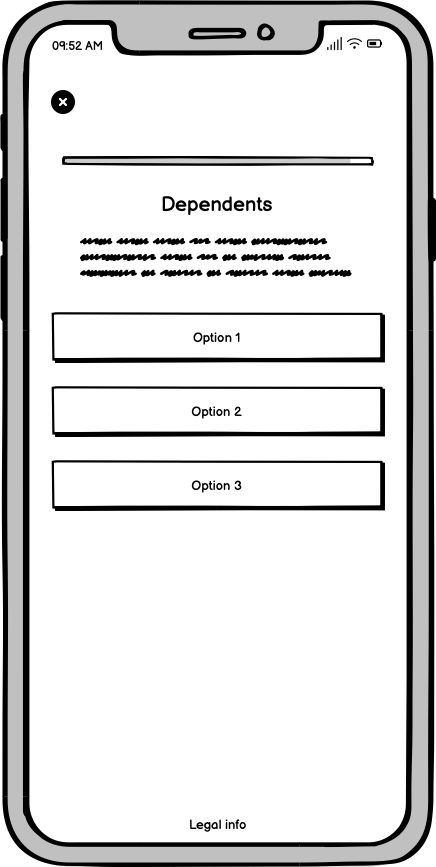

Dependents

According to regulations, the user needs to confirm their number of dependents.

-

![]()

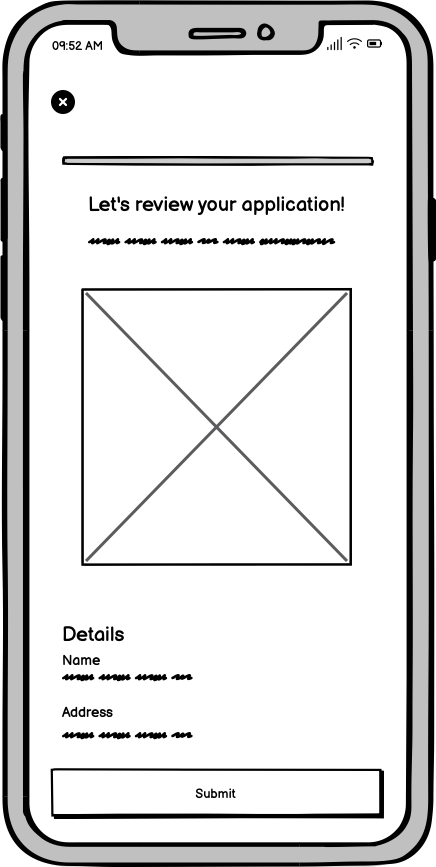

Review Screen

This screen provides an overview of the form allowing the user to amend any info.

I created a flow for the credit builder tool that addressed the target audience's needs meeting the financial institution's requirements and local laws providing a clear path towards improving their credit.

Success rate (MAU vs UEF)

The credit score builder proved to be a success, along with redesigning other functionalities. Users that requested an in-app loan grew steadily month after month, helping to consolidate the app in the regions where this feature was roll-out.

Next Project

Gaming Statistics | Betway UK